Interview with Professor Dr Bert de Groot – Head of Business Economics, Governance and Strategic Investments Program, Director Erasmus University Holding

by Annalisa Filomena – Strategy Consultant, The Decision Group

Professor dr. Bert de Groot is COO & CRFO of Erasmus Universiteit Holding BV and has several supervisory board positions. Furthermore, De Groot holds the chair of Governance and Strategic Investments. He is director of the Erasmus Executive Program The New CFO and he is director of the MSc Maritime Economics & Logistics (MEL).

De Groot has held positions at the international level in various industry sectors. Prior to his executive board and CFO position at Randstad Holding N.V. (staffing services), he was employed by Gist Brocades N.V (now DSM), the biotech and pharmaceutical company, the information management company Unisys Inc., telecom multinational KPN and Boer & Croon executive management. At Pharming N.V. (life sciences), de Groot realized corporate recovery. At AM N.V. (project development), AM was delisted, split and sold. He was CEO of Erasmus Universiteit Rotterdam Holding B.V, subsequently Rector Magnificus of Nyenrode Business Universiteit. Member of the Management Team of the Erasmus School of Economics and COO & CFRO of EUR Holding.

By 2022, the growth will come back again to be 1-3% (in real terms) per year depending on the country. 2021 will be a reset for the years to come. Make sure that your supply chain is ready for the next move and for the chosen partnerships. That has to be done now. Then put operational risk management in place with all the lessons learned.

The Breakthrough

Bert de Groot studied econometrics at the Erasmus Universiteit Rotterdam (EUR) and has followed management programs at IMD (previously IMI), Nyenrode, Wharton, INSEAD and Harvard. De Groot was awarded his PhD by the ESE at EUR for his thesis ‘Essays on Economic Cycles’.

He published on economic and business cycles, the multi-cycle structure of the economy, innovations, common-socio-economic cycle periods and dynamic stability, the thermometer of the economy and made real-time estimates of GDP growth. He made forecasts for companies and for the various market segments for the Hamburg-Le Havre ports and the Port of Rotterdam. He publishes on short- and long-term economic predictions and these are to be found in ESB, EUCLID, The New CFO linked-in, and on his linked-in. Forecasts are made for the GDP growth direction of 25 OECD countries. He published on corruption and inequality of wealth amongst the very rich and was quoted in the Harvard Journal.

In his chair Governance and Strategic Investments, he studies the decision making of the board and the behaviour of CEO’s, CFO’s and Non-Executives, from the perspective of applied psychology and financial economics. Narcissistic behaviour and the influence on decision making. Executives, CEO’s, CFO’s and Non-Executives, managers, alumni and master students participated in the studies.

In this interview, Professor de Groot will help executives and business leaders taking better decisions and picturing the future of competitiveness by looking at the present and future economic cycles.

What has happened since the outbreak of the Covid-19 pandemic?

In 2018 predictions were made on the forthcoming decline of the investment cycle and the consumer cycle to zero or lower growth of the GDP in 2020. The institutions forecasted a 3% growth. However, as of the beginning of 2019, these were in decline. The indication got only stronger since the “The 10year minus 2 years Treasury’ hit the below zero points, oct-nov 2019, indicating a crisis was about to come in 6 months. Nobody saw the Corona hit coming. I did not either. I was following the economic descent in my model and there was a difference of 3% between my two years of forecasting and those made by the Central Planning Bureau and the Dutch National Bank. The difference was remarkable.

In 2020, companies and households gradually started to change into survival mode. Investments were further reduced.

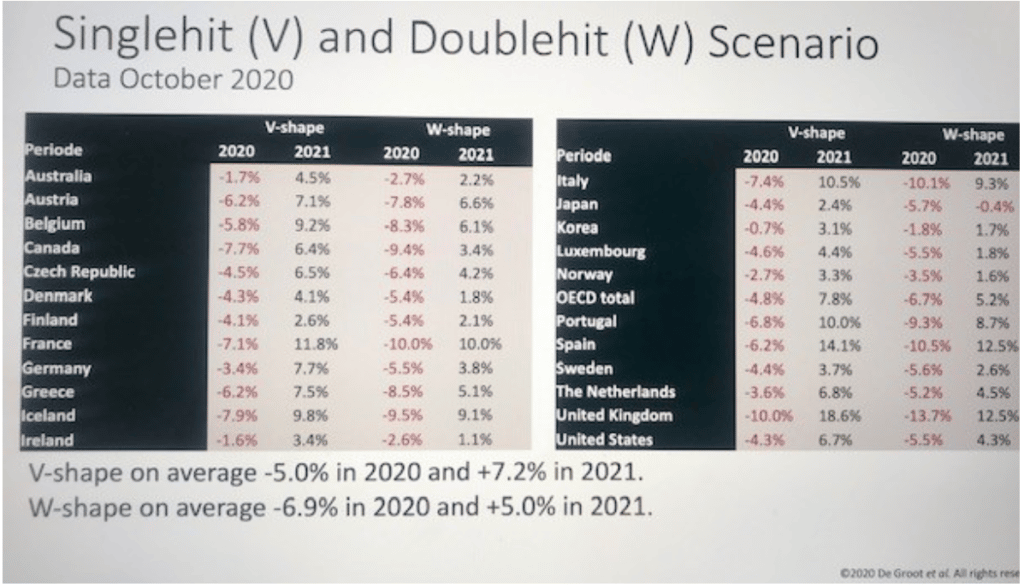

Because of the huge fiscal-financial support offered by the EU governments, companies and entrepreneurs were supported, suppressing bankruptcies and lay-offs. With the GDP’s of countries being forecasted with a V hit in 2020 (see picture 1), countries’ companies, medium and small-sized businesses and people as well suffered. Naturally, unemployment rose. The younger generations are still suffering from high unemployment rates especially in the south of Europe that got another economic crisis hit.

Due to Corona, businesses in various industries were hit in a different ways. Aircraft Companies almost faced bankruptcy and were tremendously supported by governments. Digital companies, Big Data ICT companies, on the contrary, flourished. The leisure industry, tourism, hotels, and restaurants broke down. Health Care got a rare mix of increasing Corona Care, rising death, rise of less specialized medical care in hospitals and less non-medic care because of the restrictions imposed. The staffing service companies scaled down and temporary labour suffered. Unemployment rose and because of the government support to companies, hidden unemployment remains linked to an income reduction. The school system and young people’s education suffered and there’s no doubt that the two years of reduced learning will come at a price in the future.

Innovations as such are a process where you may observe those underway breakthroughs come into the open. Starting with the r-DNA technique ( 20 years in the making) to produce vaccines, together with more digitalization, on-line spending, and video meetings software. Of course, many companies and inventors are working hard to come up with solutions and doing business in a parallel way. The new ways of doing business will be here to stay. A continuous trend is the transformation of inventions into innovations and their diffusion into products.

Problems and disruption in the supply chain became almost directly visible in various industries from the production of vaccines and medicines, to healthcare products, and car parts. As a consequence, multinational companies got a political call to insource their raw materials rather than depending on companies in other countries.

How and when will the economy pick up again?

Corona is not over yet, and it will impact EU economies until Christmas December 2021, before the level of vaccination reaches 80+ % of the population. Earlier timing is sometimes suggested, however, it remains to be seen.

I am anticipating the W shape recovery column in 2021 (see picture 1). It is less than the V-shape recovery. Over the two years, we see a shrink. Then by 2022, the growth will come back again to be 1-3% (in real terms) per year depending on the country. 2021 will be a reset for the years to come. Again, it will depend on the industry how fast the pick-up will show. Aeroplanes, transports and trains will pick up slowly, and that will take two years from now. The digital consumer companies have created more market share and smart use of ICT products are here to stay. We may see a certain stabilization of the “traditional” way of doing business that has to claw back tremendously.

Because of unemployment and lagged education, skills development also will be delayed. The government and EU investments in infrastructure, roads, bridges, and waterways will be crucial for good support. Europe lags behind €1500bln in renewal, maintenance and new investments. This is in contrast to the USA (€2000 bln is planned) and CHINA One Belt One Road initiatives both inland and internationally. The investments will have an effect on Europe competitiveness since trains bring containers in 13 days from China to Germany and the Netherlands, versus the 21 days of sea transport. The related employment in these investments will also stimulate the economy. Companies will pick up investments as well, after recalibrating their market position and R&D pipeline.

How can business leaders anticipate the directions and stay competitive?

In practical terms, I suggest to:

- Make sure that their supply chain is ready for the next move and for the chosen partnerships. That has to be done now. Then put operational risk management in place with all the lessons learned.

- Review and improve your digitalization in doing business.

- Improve the time-to-market and the way you bring products and services to the customers.

- Be bold: invest now ahead of the curve. Emphasize your sales/ marketing. You may enjoy 6 months head start.

- Understand the conditions and prerequisites on the basis of the strategic and market direction. You can easily validate your assumptions and prerequisites than outcomes of strategy in numbers in 6 -12 months’ time.

- Question Every pre-corona strategy.

- Stay close to customers’ demands, they buy products and services.

- Endorse the innovative people in your company because they know how to bring new products to the customers. Marketing strategists and R&D responsible should determine even more the deliverables and path to (new) revenues. This is because breakthroughs are anticipated in material, biological, medical and info/computer sciences. Further Technological breakthroughs are expected in nano-applications, robots, artificial intelligence, big data, biotechnology, the use of artificial materials and miniaturization.

- Personalize your products and services.

- Focus on carbon-reducing production measures and the use of environmentally friendly energy and materials.

- Endorse socially responsible ways of doing business in executive boards so as to also protect the image and reputation of the company.

How will the future look like in EU countries?

The struggles for a “one Europe” after Brexit and the productivity differences between the North and the South will continue. Political and democratic differences of opinions from all “wind- directions” will remain. Some gaps will not be closed and, economically speaking, “monetarism” will only temporarily solve the debt issue. Once the interests in the world economies and world currencies will rise again and inflation comes back to average historical average values, the problem of handling government debt will come haunting back. Interests are bound to go up in direction of 3.5 – 4.0% (100-year average). The annual fiscal budgets of the world-leading countries will show deficits. Companies will more and more be asked to take up social responsibility. How that will play out remains to be seen.

Furthermore, geopolitics will also come into play. The relationships USA-China-Korea-Japan, India-Irak-Iran and Europe-Russia will be considered. Apart from the current ongoing wars and unrest in the world for local territory, the battle for hegemony will also be playing out in the next 75 years. A grand war cycle takes approximately 144-150 years, the World War II ending in 1945 brings this cycle to an end by 2090-2095. We still have 65 – 75 years to go before the world enters into more devastating battles. The cyber wars will continue, signing the definitive paradigm shift.

With a European population of around 450 million (in 2021) people with an average age of 43 years, the age bracket around 50 years counting for the most people, 20% of its population above 65 years of age and the share of 80+ year old going up from 6% towards 15% in the rest of the millennium, we will experience a societal change. On average, three working people will pay pensions for three to two retired persons. The ageing population will change labour relations and wealth. More people will be forced to work longer than their own projected retiring age. The skilled labour Euromigration will continue on affecting societies.

On a positive note; the innovation cycle will be coming to a peak in the coming 5 -10 years. Therefore, we may experience a whole range of new product and services offerings in 8 -15 years from now. It will bring a new boost to the economy, standards of living and employment. Thinking in the long term, + 8/15 years from 2021 (2029 – 2036), there will be a more prosperous period not only for Europe. The upswing in the economy and support of new technology for many applications will have a positive effect on general health and will produce new consumer products. The skill level of professionals and the whole population will rise.

It all boils down to a philosophical question:

From the economical perspective: Do we raise productivity to let the nations and world GDP growth, and as a consequence let people, investors and workers, be more employed and make money so that they can create a living, family and be happy.

OR

From the human perspective: Do we see people as living beings finding bliss and happiness and are satisfied with their status and life?

The answer is probably intermingled: In the many research findings after happiness in this world:

- 60% was attributed to the economic wellbeing of a person or family, wealth.

- the other 40% were attributed to health, medic care, life expectancy, social cohesion, freedom of choice, being safe, education and infrastructure

15 European countries are on the top 30 list from the 156 listed countries on the World Happiness Index. The World poverty Index and the correlation “Dissatisfaction with the standard of living and GDP per capita” shows an almost inverse distribution to the happiness index. Perhaps the distribution of clean energy, clean water and distribution of technology and skills may get us in the right direction, not be slowed down by big diseases and war.

Stay tuned for the next Breakthrough Thinkers magazine Edition – The Future of Competitiveness!

Follow the Instagram page @breakthrouththinkers

Download the full magazine past edition – What Works? How the Business World is Reacting to Covid-19

Picture from the illustrator Samuel Rodriguez